Texas roof certifications: a complete homeowner guide

Texas roof certifications: a complete homeowner guide

TL;DR:

- Texas homeowners need specific roof certifications to qualify for insurance, financing, and storm resistance verification.

- There are three main certification types: government-required WPI-8, voluntary IBHS FORTIFIED, and condition/life assessments.

- Accurate timing and professional involvement are critical to avoid costly rework, insurance issues, and delays.

Texas roof certifications: a complete homeowner guide

Most Texas homeowners assume a roof certification is just a formality — a piece of paper your roofer hands over after the job is done. That assumption can cost you thousands. Get the wrong type of certification, skip the documentation process, or miss a required inspection window, and you could find yourself ineligible for wind and hail insurance, stuck in a delayed property sale, or facing denied claims after a major storm. This guide breaks down every type of roof certification used in Texas, when each one is required, how to get it, and what happens when the process goes wrong.

Table of Contents

- What is a roof certification? Types, standards, and Texas context

- When and why do Texas homeowners need roof certification?

- How the certification process works: Step-by-step for Texans

- Certification and storm resilience: Why it matters for Texas roofs

- The hidden costs of getting roof documentation wrong in Texas

- Get help with certified roof replacement in Texas

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Multiple certification types | Not all roof certifications are alike—know if you need government, third-party, or condition documentation. |

| Insurance and compliance impacts | Correct certification is often required for wind or hail insurance and during home sale or refinance in Texas. |

| Plan ahead for approvals | Start certification early in your roofing process to avoid delays or eligibility issues. |

| Storm resilience advantages | Certified roofs are proven to reduce risk and support specialized insurance and incentives. |

What is a roof certification? Types, standards, and Texas context

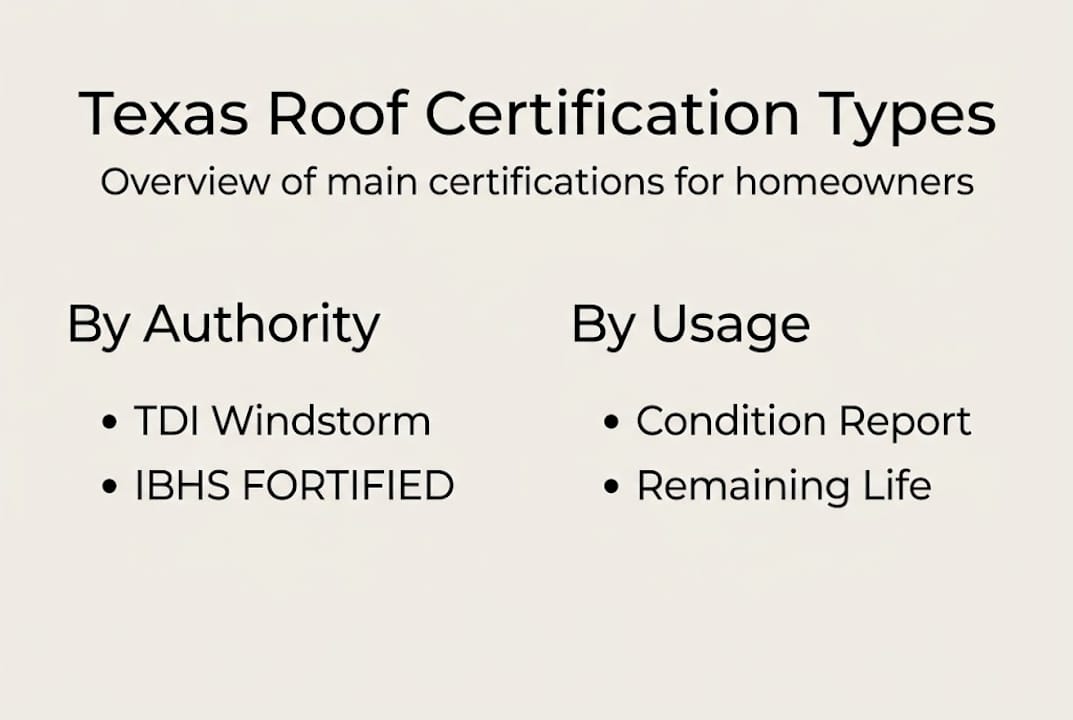

A roof certification is not one document. It is an umbrella term covering at least three distinct forms of official documentation, and confusing them is one of the most common and costly mistakes Texas homeowners make. Before you schedule any roofing work, you need to know which type your situation actually demands.

The first type is government-required windstorm compliance documentation. In Texas, this is issued by the Texas Department of Insurance (TDI) and takes the form of a WPI-8 certificate. It applies specifically to properties in designated coastal catastrophe areas and confirms that the roofing work was inspected and built to TDI’s windstorm construction standards.

The second type is program-based storm mitigation designations, most notably the IBHS FORTIFIED program. This is a voluntary upgrade designation that certifies your roof was installed using documented, verified resilience standards. It requires a third-party evaluator and a formal review by the Insurance Institute for Business and Home Safety (IBHS).

The third type is a condition or remaining-life certification, which is used primarily by insurance carriers and mortgage lenders. This is an inspector’s professional opinion on the current state of your roof and how many years of useful life remain. It can influence your eligibility for coverage or affect loan approvals.

As third-party documentation of roof condition and remaining life, certifications can influence eligibility and pricing with insurers and during real estate transactions. But the critical nuance — one most homeowners miss — is that “certification” can mean government windstorm compliance, program-based storm mitigation, or condition-based documentation, and each serves a completely different purpose.

Here is a quick comparison of the three main types:

| Certification type | Issued by | Primary use | Required or optional |

|---|---|---|---|

| WPI-8 (TDI windstorm) | Texas Dept. of Insurance | TWIA wind and hail insurance | Required in catastrophe areas |

| IBHS FORTIFIED | IBHS third-party evaluator | Storm resilience designation | Optional but incentivized |

| Condition/life certification | Licensed inspector | Insurer or lender review | Varies by lender or insurer |

Key differences between these three types include:

- Authority: WPI-8 is a government mandate; FORTIFIED is program-driven; condition certs are market-driven

- Evidence required: WPI-8 needs a TDI-approved inspector on site; FORTIFIED needs an evaluator and IBHS review; condition certs rely on a visual inspection report

- Practical use: WPI-8 gates insurance eligibility; FORTIFIED can lower premiums or unlock specialized coverage; condition certs affect loan approval or renewal eligibility

These distinctions matter enormously for two reasons. First, each certification has a different process and timeline. Second, their impact on property value and insurance access differs significantly depending on where you live in Texas.

Important: Texas is not a one-size-fits-all state when it comes to roofing compliance. A coastal homeowner in Galveston faces different documentation requirements than a homeowner in Houston or El Campo. Always confirm which type applies to your property before spending a dollar.

When and why do Texas homeowners need roof certification?

Now that you understand the different types, let’s get specific about the real-life situations where certification becomes critical. Missing the right documentation in any of these scenarios can delay your project, raise your costs, or leave you without coverage when a storm rolls through.

Insurance eligibility in coastal catastrophe areas is the most urgent scenario. In Texas windstorm-designated coastal areas, homeowners may need TDI windstorm certification (WPI-8) to qualify for TWIA wind and hail insurance after roof work. TWIA stands for the Texas Windstorm Insurance Association, and it is often the only available insurer for homeowners in high-risk coastal zones. Without a valid WPI-8, you cannot get that coverage — period.

Standard market insurance policies handle certification differently. Many private insurers require a condition or remaining-life certification before they will write or renew a policy on an older roof. If your roof is 10 or more years old, your insurer may demand documentation showing it still has meaningful life remaining. As third-party proof of condition that can influence eligibility and pricing, these certifications carry real financial weight during renewals.

Selling or refinancing your home is another major trigger. Mortgage lenders, especially those dealing in FHA or conventional loans, may require a roof inspection and certification as part of the underwriting process. If a lender believes the roof is near end of life, they can require repairs, a replacement, or a price adjustment before closing. Having an up-to-date condition certification already in hand can dramatically smooth that process.

Here is a side-by-side view of when each type of certification becomes relevant:

| Scenario | Certification type needed | Who requests it |

|---|---|---|

| Roof work in coastal TX | WPI-8 (TDI windstorm) | Required by TDI/TWIA |

| Older roof insurance renewal | Condition/life certification | Private insurer |

| Home sale or refinance | Condition/life certification | Mortgage lender |

| Seeking premium discounts | IBHS FORTIFIED | Homeowner initiative |

Other situations where certification matters:

- Filing a storm damage claim after a major weather event, especially if repairs were made without documentation

- Applying for disaster relief or FEMA assistance where proof of compliance may be requested

- Verifying work quality after hiring a contractor you are unfamiliar with

Pro Tip: Before you even schedule storm damage repair, call your insurance carrier and ask specifically which certification type they require for your property and policy. Do the same with your local authority if you are in a TDI-designated area. This one call can save you weeks of rework.

The value of a professional roof inspection before certification is also significant. An inspection helps identify issues that could prevent certification, giving you time to fix them before the official process begins.

How the certification process works: Step-by-step for Texans

Once you know which certification your situation requires, the next step is understanding how to actually get it. Each type follows a different workflow, and timing is everything — especially for government-required certifications.

For TDI/WPI-8 windstorm certification, the process goes like this:

- Confirm your property is in a designated catastrophe area. TDI publishes county and zip code lists. If your property qualifies, WPI-8 is not optional for insured roof work.

- Select a TDI-approved inspector before work begins. This is critical. The inspector must be on site during the work, not after. You cannot retroactively earn a WPI-8 on completed work that was not inspected.

- Complete roofing work to TDI windstorm construction standards. Your contractor must follow specific installation specs covering decking, underlayment, fasteners, and shingles or panels.

- Inspector submits documentation to TDI. Upon approval, TDI generates your WPI-8 record. The TDI Windstorm Inspections Program publishes and supports a WPI-8 record that homeowners can search and print online at any time.

For IBHS FORTIFIED designation, the workflow is more involved:

- Hire a FORTIFIED-trained evaluator before or during roofing work. The evaluator is responsible for documenting that specific upgrade standards are being met during installation.

- Ensure your contractor follows FORTIFIED-specific installation requirements, which go beyond standard code. These include impact-resistant shingles, sealed roof decks, and enhanced attachment methods.

- Evaluator submits documentation to IBHS, which reviews compliance against the FORTIFIED standard through an independent process. Designation is only issued after IBHS confirms all requirements are met.

- Receive your FORTIFIED designation certificate, which you can then present to insurers or use to access financial incentives.

For condition or remaining-life certifications, the process is simpler:

- Hire a licensed roof inspector or roofing contractor to perform a visual inspection

- Receive a written report documenting the roof’s current condition, estimated age, and remaining useful life

- Submit this to your insurer or lender as required

Pro Tip: Review this roof maintenance checklist before scheduling any formal inspection. Addressing minor issues like loose flashing or clogged gutters beforehand can prevent inspection failures that delay your certification.

The most important timing rule across all three types: start the documentation process before work begins, not after. Retroactive certification is either impossible (WPI-8) or significantly more complicated (FORTIFIED). Understanding the value of proactive inspections can help you plan ahead and avoid last-minute scrambles.

Certification and storm resilience: Why it matters for Texas roofs

Certification is not just paperwork. Done right, it is evidence that your roof was built or upgraded to withstand the specific weather threats Texas homeowners face. That distinction has real financial and safety consequences.

The IBHS is direct about the stakes: roof damage accounts for a large share of catastrophe-related insurance claims. When a hurricane, severe thunderstorm, or straight-line wind event hits, the roof is almost always the first point of failure. A certified, resilient roof is less likely to fail at those critical moments, which means lower personal losses and fewer insurance payouts.

But certification is not just about surviving a single storm. The FORTIFIED program, in particular, emphasizes a systems-based approach. That means it is not enough to simply use impact-resistant shingles. The documented compliance and installation verification process required for designation confirms that every layer of the roofing system, from the deck attachment to the edge metal, was installed to a higher standard. That verification step is what earns the designation and associated financial benefits. Homeowners who skip the documentation and simply use better materials do not qualify.

Here is what proper certification and storm-resilient upgrades can do for you:

- Unlock access to specialized insurance coverage, including TWIA policies in coastal areas or discounted premiums through programs that recognize FORTIFIED designation

- Reduce out-of-pocket storm losses by minimizing damage that falls below your deductible or that coverage excludes

- Increase your home’s marketability by demonstrating documented compliance with recognized resilience standards

- Protect your family by ensuring the roof performs as designed during a major weather event

Proper weatherproofing goes hand in hand with certification. A roof that meets or exceeds documented standards is far more likely to stay watertight and structurally sound through the kind of intense heat, hail, and hurricane-force winds that define Texas weather seasons.

The bottom line: Certification signals to your insurer, your lender, and your buyer that the roof is not just aesthetically sound — it is structurally verified. That distinction affects how weather impacts roofing durability over time and how much the roof costs you to own.

The hidden costs of getting roof documentation wrong in Texas

Here is something most roofing guides will not tell you: the most common certification mistake is not skipping it entirely. It is getting the wrong type, in the wrong order, with the wrong professional involved.

We have seen homeowners pay for a condition certification when their insurer actually required a WPI-8. We have seen others install FORTIFIED-eligible materials and then discover they cannot receive the designation because no evaluator was on site during installation. That mistake is impossible to fix without tearing off and redoing the work.

The risks extend beyond wasted money. If you complete roof work in a TDI catastrophe area without a WPI-8, your TWIA coverage can be voided for that work. A denied wind or hail claim after a major storm can mean tens of thousands of dollars in out-of-pocket repairs. Delays in property sales caused by missing lender-required certifications can cost you a buyer entirely.

Our advice is simple but specific: before you sign with any contractor, confirm with your insurance carrier exactly which certification they require for your policy and property location. Then confirm with TDI or your local authority whether your area mandates government windstorm compliance. Finally, make sure the roofer you hire understands how to work within that documentation framework. Knowing how roofers interact with insurance claims can help you ask the right questions during that vetting process.

Get help with certified roof replacement in Texas

Navigating Texas roof certification requirements is genuinely complex, and the consequences of getting it wrong are too costly to risk. Working with a roofer who understands the TDI windstorm process, the FORTIFIED documentation workflow, and what lenders and insurers actually need makes the difference between a compliant, covered roof and an expensive paperwork nightmare.

At Mister ReRoof, we handle certified roof replacements across the Houston and El Campo areas, including metal roof replacement in Victoria and shingle roof replacement in Hallettsville. We work with homeowners to ensure every replacement meets the documentation requirements their insurer, lender, and local authority demand. Contact Mister ReRoof today for a free estimate and a clear plan for getting your roof certified right the first time.

Frequently asked questions

What is a WPI-8, and when is it required in Texas?

A WPI-8 is a TDI-issued windstorm certification required for insurance eligibility after roof replacements or repairs in Texas coastal catastrophe areas. Properties in designated areas must have TDI-inspected work to qualify for TWIA wind and hail coverage.

Is a FORTIFIED roof certification necessary for all Texas homes?

FORTIFIED certification is optional but provides recognized proof of storm-resistant improvements and can lead to financial incentives, especially in storm-prone areas. Designation requires documented compliance verified by a third-party evaluator and reviewed by IBHS.

How do roof certifications affect home insurance pricing?

A roof certification offers third-party proof of roof condition, which can help qualify for coverage or better premiums depending on the insurer. Certifications can influence eligibility and pricing with insurers during renewals and real estate transactions.

How can I print or access my Texas roof certification?

For TDI/WPI-8 certifications, you can search and print your record online through the TDI Windstorm Inspections Program. The TDI program publishes WPI-8 records that homeowners can access at any time.

Can a missing certification cause my insurance to be denied?

Yes, lacking the required certification can mean you are ineligible for certain wind and hail insurance policies in designated Texas areas. In windstorm contexts, missing certification affects insurance eligibility entirely, not just premium pricing.