TL;DR:

- Replacement cost value roofing pays the full current price to repair or replace a roof without deducting for age or wear. It involves a two-stage payout process where insurers provide an initial ACV payment and a second payment after repairs are documented and completed. Property owners should regularly review their policies, document damage thoroughly, and understand their coverage type to maximize claim benefits.

Replacement cost value (RCV) roofing is defined as insurance coverage that pays the full current price to repair or replace your damaged roof without deducting for age or wear. The Texas Department of Insurance contrasts RCV directly with actual cash value (ACV), which reduces your payout based on how old or worn your roof is. For property owners and managers, understanding what is replacement cost value roofing is the difference between a claim that covers your full repair bill and one that leaves you thousands short. This guide breaks down how RCV works, how it compares to ACV, what roof replacement costs to expect, and how to protect your coverage long term.

What is replacement cost value roofing in insurance claims?

RCV roofing coverage means your insurer pays to restore your roof to its pre-damage condition using like-kind materials at current market prices. No depreciation is subtracted. If a hailstorm destroys your 10-year-old shingle roof, the insurer prices the replacement as if you are buying and installing that roof today, not at what a 10-year-old roof is worth on paper.

The industry term for this concept is “replacement cost value,” sometimes also called “new for old” coverage. PropertyCasualty360 describes it as reimbursing the actual current cost to restore the roof rather than its depreciated value. That framing helps clarify why RCV policies carry higher premiums. You are paying for the right to receive a full restoration, not a discounted settlement.

One critical boundary: insurance only covers damage caused by a covered event such as a storm, fallen tree, or accident. Normal aging, gradual wear, and deferred maintenance are not covered, even under RCV policies. A roof that simply reaches the end of its lifespan does not qualify for an RCV claim.

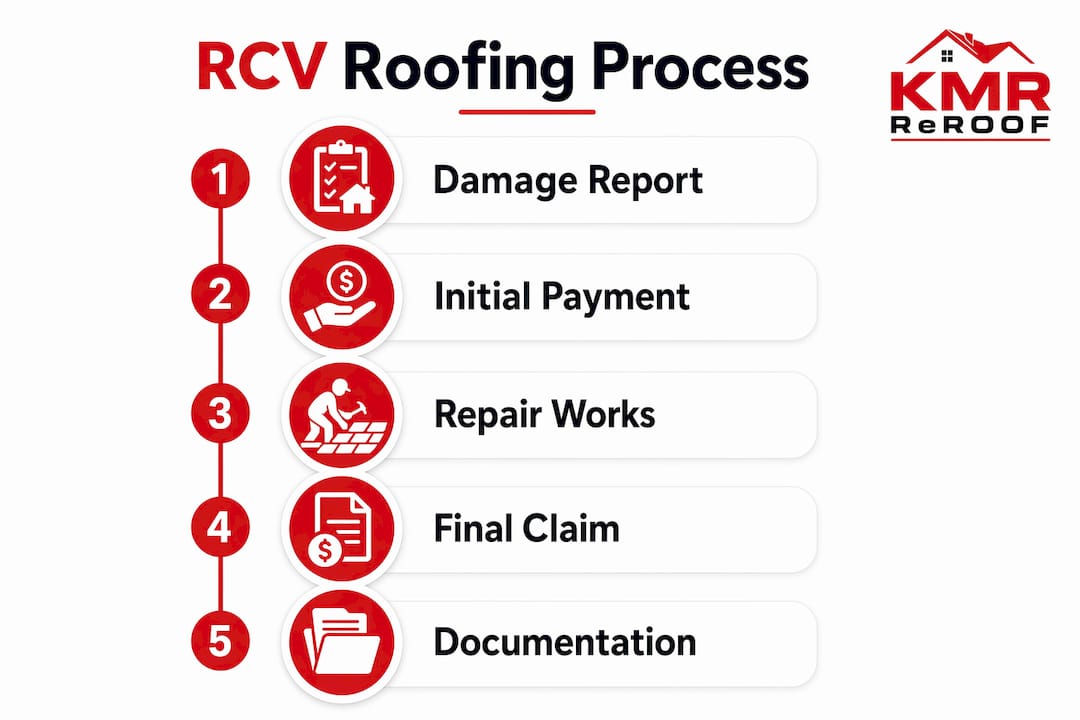

How the two-stage payment process works

RCV claims do not pay out in a single check. Insurance pays in two stages: first, an initial partial payment based on the ACV of the damage, then a second payment covering the remaining balance once repairs begin or are completed. The gap between those two checks is called recoverable depreciation.

Here is the typical sequence:

- You file a claim and an insurance adjuster inspects the damage.

- The insurer issues a first check equal to the ACV of the repair.

- You hire a licensed contractor and begin or complete the work.

- You submit proof of repairs and invoices to the insurer.

- The insurer releases the second check covering the recoverable depreciation.

Pro Tip: Never cash the first check and assume the claim is closed. Submit your contractor invoices and repair documentation promptly to unlock the second payment. Missing the insurer’s deadline forfeits that money permanently.

RCV vs. ACV roofing coverage: which one do you have?

The core difference between RCV and ACV roofing coverage is whether depreciation is subtracted from your claim payout. ACV deducts depreciation based on your roof’s age and condition. RCV does not. On a 15-year-old roof with $20,000 in storm damage, an ACV policy might pay $8,000 after depreciation. An RCV policy pays the full $20,000 replacement cost.

The tradeoff is premium cost. RCV coverage costs more and may not even be available for older or poorly maintained roofs. Insurers sometimes switch policies from RCV to ACV at renewal when a roof reaches a certain age, often 15–20 years depending on the carrier and material.

| Feature | RCV Coverage | ACV Coverage |

|---|---|---|

| Depreciation deducted | No | Yes |

| Claim payout | Full replacement cost | Depreciated value |

| Premium cost | Higher | Lower |

| Best for | Newer roofs, full protection | Older roofs, budget premiums |

| Availability | May be denied for aging roofs | Generally available |

Key points to keep in mind when comparing the two:

- Newer roofs (under 10 years) almost always qualify for RCV coverage.

- Older roofs may be forced onto ACV terms at renewal, regardless of condition.

- Switching from ACV to RCV depends on your roof’s age and your insurer’s underwriting rules.

- RCV leads to significantly higher claim payouts but requires meeting repair and documentation conditions before the full amount is released.

If you are unsure which coverage you carry, pull your insurance declarations page and look for the words “replacement cost” or “actual cash value” next to your roof coverage. Do not assume. Many property owners discover they have ACV only after filing a claim.

How to calculate roofing replacement cost for budgeting

Accurate roofing cost estimates matter for two reasons: they help you budget for a replacement project, and they give you a realistic benchmark when reviewing your insurance settlement offer. The two numbers are related but not identical.

Installed roof replacement costs run roughly $4–$11 per square foot depending on materials and complexity. That range reflects a wide spread in material costs, from basic three-tab asphalt shingles at the low end to standing-seam metal or slate at the high end. Labor, roof pitch, and local market rates all push the final number up or down.

| Roofing Material | Installed Cost Range (per sq ft) | Typical Lifespan |

|---|---|---|

| Asphalt shingles | $4–$7 | 20–30 years |

| Architectural shingles | $5–$9 | 25–40 years |

| Metal (standing seam) | $8–$14 | 40–70 years |

| TPO (flat roofs) | $5–$10 | 15–30 years |

| Slate or tile | $10–$30 | 50+ years |

Insurance adjusters use local current pricing and comparable materials to calculate your claim settlement. That means the adjuster’s number and your contractor’s bid should be in the same ballpark. If they are not, you have the right to dispute the estimate with documentation.

Pro Tip: Get at least two written contractor estimates before accepting an insurance settlement. Detailed bids that specify materials, labor, and square footage give you leverage if the adjuster’s number comes in low. Keep photos of your roof’s condition taken annually, not just after damage.

For Houston-area property owners, you can use Misterreroof’s roof cost estimating guide to build a realistic baseline before you ever file a claim.

What property owners and managers should do right now

Managing RCV roofing coverage well requires more than picking the right policy. It requires ongoing attention to your roof’s condition, your policy terms, and your claim process.

- Review your declarations page every renewal. Insurers may adjust coverage as your roof ages, quietly switching you from RCV to ACV without a separate notice beyond the renewal documents.

- Schedule annual roof inspections. Documented maintenance records show your insurer the roof has been cared for, which supports both coverage eligibility and claim accuracy.

- File claims promptly after covered events. Delayed claims invite disputes about whether damage was pre-existing or storm-related.

- Coordinate with a licensed roofing contractor early. Contractors experienced with Texas insurance claims know how to document damage in the format adjusters require, which speeds up the two-stage payment process.

- Track your recoverable depreciation deadline. Failure to submit proof of completed repairs on time can cause permanent loss of the second payment. Ask your insurer for the exact deadline in writing.

- Understand your roof’s age relative to your policy. If your roof is approaching 15 years, ask your insurer now whether your RCV coverage will be maintained or converted at the next renewal.

One often-overlooked step: after any major storm, document the damage yourself with dated photos before any repairs begin. That record becomes part of your claim file and protects you if the adjuster’s visit is delayed. Misterreroof’s storm damage workflow guide walks through exactly how to do this for Texas homeowners.

Key takeaways

Replacement cost value roofing coverage pays the full current cost to restore your roof without depreciation, but only if you complete repairs, document them properly, and meet your insurer’s claim deadlines.

| Point | Details |

|---|---|

| RCV definition | RCV pays full current replacement cost with no depreciation deducted from the claim. |

| Two-stage payment | Insurers release a partial first check, then the balance after repairs are documented. |

| RCV vs. ACV gap | ACV deducts depreciation; on older roofs, the payout difference can be thousands of dollars. |

| Cost benchmarks | Installed replacement costs run $4–$11 per square foot depending on material and complexity. |

| Policy vigilance | Review your declarations page every renewal to confirm you still carry RCV, not ACV. |

The fine print matters more than the label

Most property owners hear “replacement cost coverage” and assume they are fully protected. The reality is more conditional than that. I have seen owners lose thousands in recoverable depreciation simply because they did not know a second check existed, let alone that it required documented proof of completed repairs.

The two-stage payment process is the part of RCV coverage that catches people off guard. The first check feels like a settlement. It is not. It is a deposit. The real payout comes after you do the work and submit the paperwork. Miss the deadline and that money is gone.

What I find equally underappreciated is how much documentation quality affects claim outcomes. Contractor estimates and photos anchored to local current pricing are not just helpful. They are your primary tool for disputing a low adjuster estimate. A contractor who understands the insurance claim process is worth more than one who simply offers the lowest bid.

The other hard lesson: do not wait for damage to review your policy. By the time a storm hits, it is too late to upgrade from ACV to RCV. Check your declarations page today, confirm your coverage type, and ask your insurer directly what happens to your RCV eligibility as your roof ages. That one conversation can save you a five-figure gap between what you expect and what you receive.

— Misterreroof

Get expert roof replacement help in texas

Understanding your coverage is only half the equation. The other half is working with a contractor who knows how to execute a replacement that satisfies both your insurer and your property’s long-term needs.

Mister Reroof serves property owners across El Campo, Houston, and surrounding Texas communities with professional roof replacement for shingle, metal, flat, and TPO systems. Every project is documented to support insurance claims and built to handle Texas weather. If you are navigating a claim or planning a proactive replacement, start with Misterreroof’s Texas roof replacement guide for step-by-step guidance aligned with insurance requirements. You can also explore Houston replacement tips for practical advice specific to the local market. Contact Misterreroof today for a free estimate.

FAQ

What does replacement cost value mean for roofing?

Replacement cost value means your insurer pays the full current cost to replace your damaged roof using comparable materials and labor, with no deduction for the roof’s age or prior condition.

How is RCV different from actual cash value for a roof?

RCV pays the full replacement cost without depreciation. ACV subtracts depreciation based on roof age and wear, which can reduce your payout significantly on an older roof.

Does RCV roofing insurance pay out in one check?

No. RCV claims pay in two stages: an initial partial payment based on ACV, then a second payment covering recoverable depreciation after repairs are completed and documented.

How much does roof replacement cost for insurance purposes?

Installed replacement costs range from $4–$11 per square foot depending on materials, roof complexity, and local labor rates. Insurance adjusters use local current pricing to calculate claim settlements.

Can my insurer switch me from RCV to ACV coverage?

Yes. Insurers may convert RCV to ACV at renewal as your roof ages, typically when it reaches 15–20 years. Review your declarations page every renewal to confirm your current coverage type.